Apr 01, 2025

0% APR vs Cash Back: Which Is Better for Leasing a New Car?

Oct 03, 2025

When you walk into a dealership and shop for new cars for lease, the salesperson will often ask you to choose between two common incentives: cash back and low interest rates. Manufacturers use these promotions either to move last-year model inventory or to make competitive models more attractive — and dealers will naturally try to steer your choice toward the option that fits their margins.

Both incentives can save you a meaningful amount of money, but you can’t usually take both. So the question becomes: what’s more advantageous — cash back vs low APR? Since the discounts work in fundamentally different ways, the right choice can be obvious in some cases and subtle in others. A 0% financing offer is typically available only to buyers with excellent credit or those who can handle a higher short-term payment, while cash back reduces the vehicle price and lowers the amount you need to finance.

If you’re weighing these options and want to compare 0% APR vs cash back, I’ll walk you through the steps: understand how each incentive works, evaluate your financial profile, compare specific deals, and calculate total costs for each option.

What you’ll learn in this article:

- What cash back actually is and its pros and cons

- What 0% APR means and why it isn’t available to everyone

- How to compare special financing vs cash back to determine which is better for you

- Which factors affect the final decision

- Expert tips to avoid overpaying

What is Cash Back in Leasing a Car?

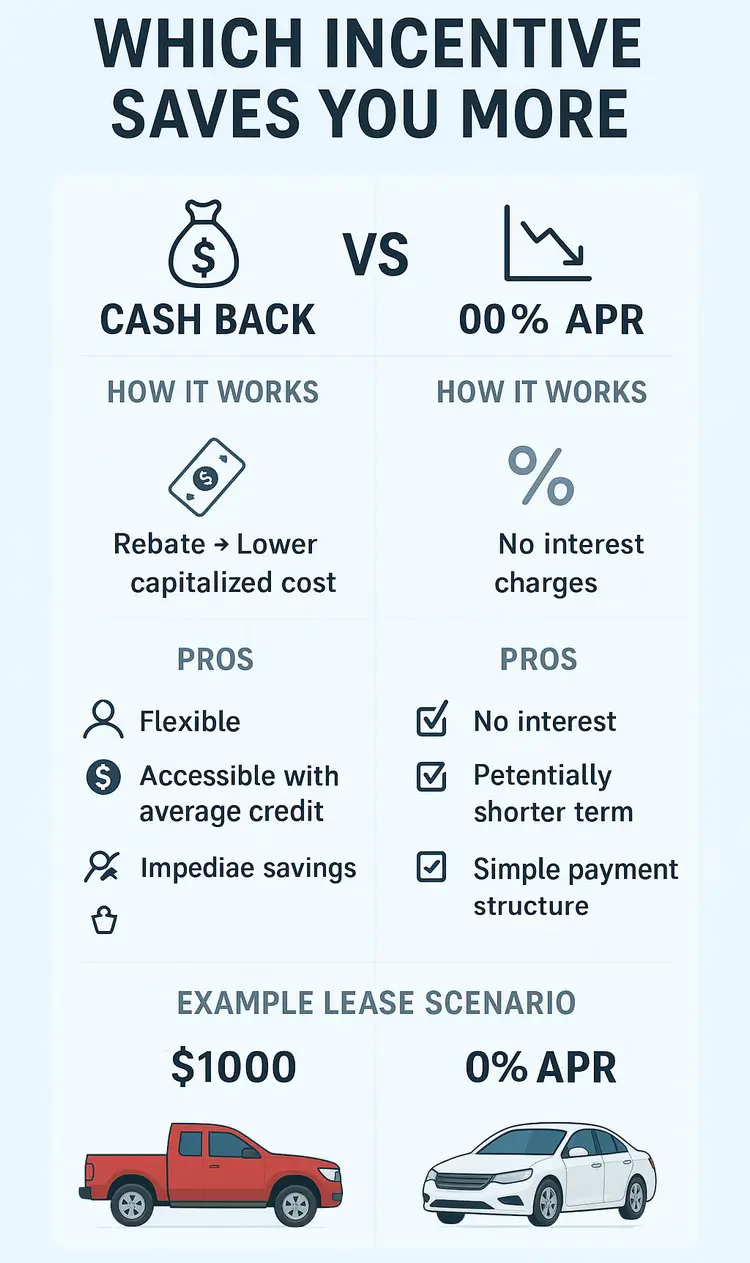

The term cash back sounds like you’ll walk away with a check in your pocket — but in practice it usually works differently. In leasing, cash back is typically a manufacturer rebate that reduces the vehicle’s price or, in lease terms, the capitalized cost.

Manufacturers and dealerships may label these incentives variously as bonus cash, rebate, customer cash, or purchase allowance, but the effect is the same: the rebate reduces the deal’s effective price. Occasionally a buyer can receive an actual check, but more commonly the rebate is applied up front to reduce the capitalized cost.

Most cash back incentives range from $1,000 to $2,000, though some can be much larger — up to $5,000 on trucks or premium models. Such rebates can often make a higher-trim or better-equipped vehicle more affordable.

How Cash Back Works

It’s important to note that these discounts are available only when you lease or buy directly from an authorized dealer. The rebate is usually processed as part of the deal, either applied as part of your down payment (you can calculate its effect on your monthly payment with a down payment calculator) or directly deducted from the vehicle’s selling price.

To understand how this works in practice, here’s a simple example:

Suppose a new crossover has an MSRP of $35,000, and the manufacturer offers a $2,000 rebate. With the rebate applied, your adjusted capitalized cost drops to $33,000. For a lease, that means all subsequent calculations (residual value, monthly payments) are based on the lower amount. As a result, your monthly lease payment decreases, and your overall cost of ownership goes down.

Keep in mind, though, that a rebate is not the only way to reduce the cost of a deal. You can often secure an even better offer through effective negotiation — lowering dealer fees, or negotiating extras like floor mats or complimentary maintenance for the entire lease term.

Important: Although cash back reduces the vehicle’s price, in most states sales tax is calculated on the full pre-rebate price. This means your tax bill may end up higher than you initially expect.

Advantages and Disadvantages of Bonus Cash

Cash back incentives come with both strengths and limitations. To make it easier to compare, here’s a breakdown of the key pros and cons:

| Pros | Cons |

|---|---|

| Flexibility: can be applied toward the down payment, and in some cases even issued as a check | May require financing through the manufacturer’s captive finance company (often at less competitive rates) |

| Accessible with average credit: does not demand the top-tier credit score usually required for 0% APR offers | Does not always reduce the taxable base — depends on state tax laws |

| Immediate savings: the cost of the deal is reduced from day one | Limited to certain models and trims, and promotions are not always available |

When Does Cash Back Make Sense?

A cash incentive is often easier to qualify for than special financing, so if your credit history does not meet the strict requirements for 0% APR, it may be your only option. But rebates can be especially attractive in the following cases:

- You plan to make a significant down payment or use a trade-in to reduce the financed amount.

- The manufacturer is offering a generous rebate (e.g., $3,000–$5,000), which in total savings may outweigh the interest you’d avoid with low-APR financing.

What Does 0% APR Mean?

The phrase “0% APR” sounds almost like free money — as if you’re leasing or financing a car with no extra costs. In reality, it’s a special financing offer in which the manufacturer eliminates interest charges, allowing you to pay only the “pure” cost of the vehicle. In leasing terms, the customer pays for depreciation plus the rent charge.

Important: 0% APR does not exempt you from taxes and mandatory fees. It only means there are no finance charges.

How 0% Financing Works

The principle is simple: your entire payment goes toward covering the vehicle’s use, with no interest added. This can save you thousands of dollars, since typical finance charges might add $2,000, $3,000, or more over the term of a lease or loan.

For example:

- Suppose you choose a vehicle with an MSRP of $30,000.

- At a market rate of 4.77% over 36 months, you would pay roughly $2,570 in interest alone.

- With 0% APR, you pay only the depreciation (the difference between the vehicle price and residual value), with no additional finance charges.

It’s worth noting that in leasing, offers of a true 0% APR equivalent (zero money factor) are rare. More commonly, you’ll see low-interest promotions in the range of 2%–4% APR for 48–72 months. The savings compared to cash back will vary greatly depending on the rate, the lease term, and the specific offer. And these programs usually come with restrictions — a limited selection of models, shorter terms, and strict credit score requirements.

Advantages and Disadvantages of 0% APR

Just like with bonus cash, special financing programs under 0% APR come with their own nuances.

First, zero-interest financing is usually available only for certain makes, models, trims, or specific model years — much like rebate promotions. Second, such offers are typically reserved for customers with excellent credit (high FICO scores). Finally, the lease term is often limited to shorter periods, which can constrain monthly payment options.

Here’s a side-by-side look at the main pros and cons of 0% APR:

| Pros | Cons |

|---|---|

| No interest charges: your payments go only toward the vehicle’s depreciation | Strict credit score requirements (often FICO 720+) |

| Optimal term length: usually 36–48 months | Rarely extend beyond three years, which limits flexibility in lowering monthly payments |

| Potentially lower monthly payments: with the same lease term, the absence of interest can make payments lower than with a rebate offer | Applies only to new vehicles from a limited selection of models |

When Does 0% APR Make Sense?

A 0% APR lease or financing deal can be the better choice in these situations:

- You have a stable income and a high credit score (typically 700–720 or above).

- Your main goal is to minimize total finance costs.

- You are comfortable with the models available under the promotion and primarily need a reliable car for everyday commuting.

Cash Back vs. Low APR Deals: Where’s the Bigger Savings?

When a manufacturer asks you to choose between cash back vs. low APR, the decision is not always straightforward. It all depends on the numbers: the size of the rebate, the interest rate, and the lease terms. Let’s break down two scenarios to see where the savings really come from.

Lease Terms for Comparison:

- MSRP: $35,000

- Residual Value 55%: $19,250

- Term: 48 months

Example 1 — Small Rebate ($1,000)

Let’s calculate the total lease cost over the full term.

Scenario A — $1,000 Cash Back + Standard Rate (4.77% APR ≈ Money Factor 0.0020)

- Cap Cost = $34,000

- Depreciation = (34,000 − 19,250) ÷ 48 ≈ $306/month

- Finance Charge = (34,000 + 19,250) × 0.0020 ≈ $106/month

- Total Monthly Payment ≈ $412

- Total Lease Cost ≈ $19,776

Scenario B — 0% APR (Money Factor = 0)

- Cap Cost = $35,000

- Depreciation = (35,000 − 19,250) ÷ 48 ≈ $328/month

- Finance Charge = $0

- Total Monthly Payment ≈ $328

- Total Lease Cost ≈ $15,744

Conclusion: With a small rebate ($1,000), 0% APR is far more advantageous — saving you over $4,000 across the lease term.

Example 2 — Large Rebate ($5,000)

Now let’s see how things change when the manufacturer offers a generous rebate.

Scenario A — $5,000 Cash Back + 4.77% APR (MF 0.0020)

- Cap Cost = $30,000

- Depreciation = (30,000 − 19,250) ÷ 48 ≈ $224/month

- Finance Charge = (30,000 + 19,250) × 0.0020 ≈ $98/month

- Total Monthly Payment ≈ $322

- Total Lease Cost ≈ $15,456

Scenario B — 0% APR (Money Factor = 0)

- Total Lease Cost = $15,744 (unchanged)

Conclusion: With a large rebate ($5,000), cash back wins. Monthly payments are lower, and the total savings amount to about $288 over the lease term.

Summary Table

| Scenario | Cash Back | 0% APR | Winner |

|---|---|---|---|

| Rebate $1,000 | $412/mo, $19,776 total | $328/mo, $15,744 total | 0% APR |

| Rebate $5,000 | $322/mo, $15,456 total | $328/mo, $15,744 total | Cash Back |

Key Takeaways

- With smaller rebates, 0% APR almost always wins.

- With larger rebates (several thousand dollars), the reduction in capitalized cost can make cash back more attractive.

- However, keep in mind: 0% APR deals are often limited to shorter terms (24–36 months). While they reduce total cost, the shorter lease period can result in higher monthly payments compared to a longer lease with a rebate.

You can always check the latest Best Lease Deals section to see which models currently offer either strong rebates or 0% APR promotions.

Why It’s Important to Do the Math Yourself

Every deal is unique: models, rates, and incentives differ between manufacturers. That’s why it’s always worth using a low APR vs. cash back calculator. Such a tool lets you quickly compare both scenarios — one with a rebate and one with 0% APR — and see which option delivers the real savings in your situation.

Expert tip: Don’t rely solely on the dealer’s pitch. Ask to see two breakdowns:

- one with cash back + standard interest;

- the other with 0% APR (or the special rate offered by the manufacturer).

Compare the total lease cost, not just the monthly payment. Only then will you see which option is truly more cost-effective.

How to Secure a Good Deal

Here are three practical tips to make sure you sign the best lease contract:

- Always negotiate. In the U.S., bargaining is expected. First, negotiate the lowest possible price, then apply either the rebate or special financing.

- Focus on total cost, not just the payment. Always compare the total lease cost, including taxes and fees, instead of getting distracted by a “low monthly payment.”

- Understand taxes and fees. In most states, sales tax is calculated based on the full vehicle price before the rebate is applied. But there are exceptions: in states like Arizona, California, Michigan, Ohio, Texas, and Utah, the rebate can also reduce the taxable amount. In these states, cash back delivers an extra tax advantage.

Final Thoughts

There’s no one-size-fits-all answer to the question: cash back vs. 0% APR — which is better? It all depends on your financial situation:

- 0% APR is best if you have an excellent credit score and want to minimize finance charges.

- Cash back is more flexible: easier to qualify for with an average credit profile and especially attractive when the rebate is large.

- In states where rebates reduce the taxable amount (for example, California or Texas), cash back can be particularly advantageous.

The golden rule: don’t trust the advertisement alone. Run the numbers with a calculator, compare both offers side by side, and pick the one with the lower total cost.

Frequently Asked Questions

0% APR or cash back — which is better?

It depends on the deal and your credit profile. The only way to know is to calculate both options.

Why are low interest rates good?

Because they reduce the amount you overpay for financing, making the total cost of leasing a car lower.

When do manufacturers usually offer cash back?

The most generous rebates typically appear at the end of the calendar year, during clearance sales of outgoing model-year vehicles, or on cars with weaker demand.

Trending post

1

4