Apr 01, 2025

What Is Money Factor on a Lease and How to it Affects the Deal: Explanation, Conversion and Comparison

Jul 04, 2025

Understanding the Money Factor in Leasing: A Key to Smarter Auto Lease Decisions.

When leasing a vehicle, one of the most important — and often misunderstood — terms you'll encounter is the money factor (MF). This small number directly determines the interest portion of your monthly lease payments. Even a slight change in the money factor can cost — or save — you thousands of dollars over the term of your lease.

In this guide, you’ll learn:

- What the money factor is and how it’s used in lease calculations

- How to compare the money factor to APR

- How to convert the money factor into an APR

- How to calculate your lease’s money factor

- Who sets the money factor and what influences it

- What is considered a “good” or “bad” money factor

- How to spot red flags in lease offers

- Final Thoughts

By the end of this article, you’ll clearly understand how the money factor works, how it affects the overall cost of your lease, how to use a lease money factor calculator to your advantage, and how to negotiate like a pro. You'll be able to make sure you're getting the best deal possible. I’ll also answer the most frequently asked questions about lease financing.

What Is the Money Factor in a Lease?

The money factor is essentially the interest rate you pay to finance a leased vehicle over the term of the lease. Unlike traditional auto loans, where the rate is expressed as an Annual Percentage Rate (APR), leases use a decimal format — typically something like 0.00125 or 0.00275.

Although this decimal format might seem less intuitive at first glance, it still reflects the cost of borrowing money to lease the vehicle. Most importantly, the money factor is part of the formula used to calculate the finance charge (often labeled as lease charge in your contract), which — along with depreciation and taxes — determines your total monthly lease payment.

This factor represents the lender's expected earnings from financing the lease. And because many customers don’t fully understand it, the money factor is often a gray area in auto leasing — one that dealers can use to build in hidden profit margins.

How the Money Factor and APR Impact the Cost of a Car Lease

Your monthly lease payment is based on several key components, including:

- MSRP (Manufacturer’s Suggested Retail Price)

- Selling Price (the negotiated purchase price)

- Residual Value (the estimated value of the vehicle at the end of the lease term)

- Depreciation (the difference between the selling price and the residual value)

- Finance Charge (calculated using the money factor or APR)

- Lease Term (the number of months in the agreement)

One of the most significant components of your monthly payment is the finance charge, which is determined using the money factor. The formula is as follows:

Monthly Finance Charge = (Cap Cost + Residual) × Money Factor

The capitalized cost (Cap Cost) is the final amount you're financing through the lease, after applying discounts, trade-in credits, and any down payment.

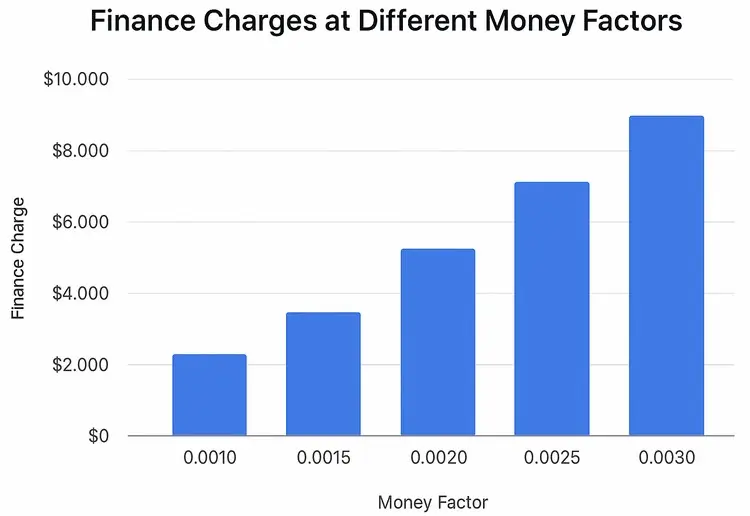

The money factor on lease plays a central role in shaping your base monthly payment. The higher your MF, the more you’ll pay in finance charges. Even a small difference — say, 0.0020 vs. 0.0025 — can add hundreds or even thousands of dollars to the total cost of your lease.

That’s why it’s critical to understand how this figure works before you sign your lease agreement.

Money Factor vs. APR: What’s the Difference?

One of the most common questions from consumers is: What’s the difference between APR and the money factor? The confusion often stems from the fact that they are presented differently — APR is typically expressed as a percentage, while the money factor is written as a decimal.

For example:

- APR = 6%

- Money Factor = 0.0025

Despite the different formats, both represent the cost of financing. The money factor is the cost of financing your lease payments, while the APR is the cost of borrowing money to buy a vehicle.

The money factor is the standard way to express lease finance charges. But if you're more familiar with annual percentage rates, converting the money factor into an APR is quick and helpful.

How to Convert Money Factor to APR

In most lease deals (unless it's a promotional offer like 1.9% APR), the interest rate isn't presented as an APR — you’ll usually see the money factor instead, if it’s disclosed at all.

To understand how much interest you're actually paying, you can convert the money factor to an APR using a standard multiplier: 2400. This factor reflects the 12-month nature of annual interest and the fact that lease interest is charged on the sum of the capitalized cost and residual value.

This conversion makes it easier to compare leasing costs to those of traditional auto loans.

APR vs. Money Factor

To convert a money factor into an annual percentage rate (APR), simply multiply it by 2400:

APR = Money Factor × 2400

Example:

APR = 0.0027 × 2400 = 6.48%

To convert APR back to a money factor:

Money Factor = APR ÷ 2400

Understanding this relationship lets you approximate the lease’s effective interest rate and compare it with other financing options.

How to Calculate the Money Factor from a Lease Offer

If you've received a lease offer and want to determine the money factor, you can use the following formula:

Money Factor = Lease Charge ÷ ((Cap Cost + Residual) × Lease Term)

Where:

- Lease Charge — total finance charges over the full term of the lease

- Cap Cost — agreed-upon price of the vehicle (capitalized cost)

- Residual Value — estimated value of the car at the end of the lease

- Lease Term — duration of the lease in months

You can use a lease money factor calculator, Google Sheets, or Excel to simplify this calculation — especially useful when comparing multiple lease offers.

Example:

- Vehicle Price: $35,000

- Residual Value: $18,000

- Lease Term: 36 months

- Total Lease Finance Charges: $4,500

Calculate Money Factor using the formula: $4,500 ÷ (($35,000 + $18,000) × 36)

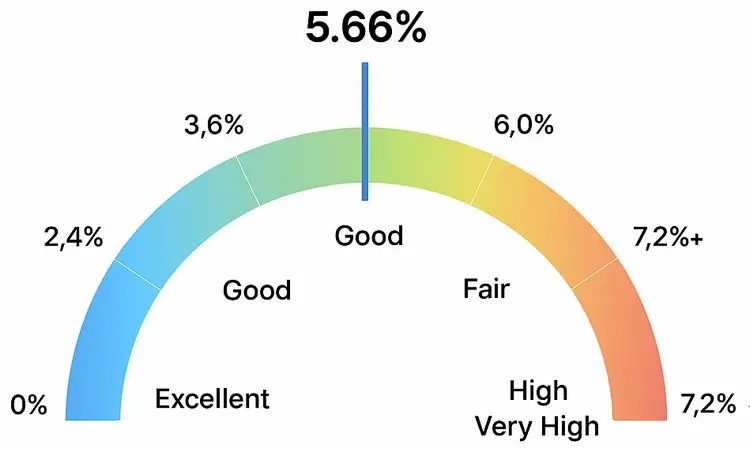

Money Factor = 0.00236

Equivalent APR ≈ 5.66%

Want to estimate your monthly finance charge? Use this formula:

Finance Charge = (Cap Cost + Residual Value) × Money Factor

Example:

($35,000 + $18,000) × 0.00236 = $125.08/month

Total Finance Charges = $125.08 × 36 = $4,502.88

Why You Should Convert the Money Factor to APR — And When It Matters Most

Most consumers are more familiar with APR than with money factors. Converting the money factor to an APR helps you:

- Compare lease offers to traditional financing deals

- Determine whether your rate is fair

- Understand the true cost of borrowing

Rather than calculating it manually, you can use online tools or a money factor to APR calculator to instantly convert and assess any lease offer.

Who Sets the Money Factor?

The money factor in a lease agreement is not set by the dealer. Instead, it's determined by the lender or leasing company, based on several key factors:

- Your credit score (FICO): Higher credit scores typically qualify for lower money factors (and lower interest rates).

- Lease term: Longer lease terms often come with slightly lower money factors.

- Vehicle type and market demand: Luxury or high-demand models tend to have higher money factors.

- Residual value: Vehicles with higher residual values (less depreciation) often come with lower money factors.

- Manufacturer incentives: Lease deals subsidized by automakers can reduce the money factor significantly.

Your credit score is the single most important factor. Less risk to the lender means a better rate for you. Leasing companies group customers into credit tiers, and each tier corresponds to a different money factor range. The better your credit, the lower the factor.

How Dealers Can Mark Up or Discount the Money Factor

While the dealer doesn’t set the base money factor (known as the “buy rate”), they can mark it up for additional profit or lower it slightly as part of a discount or promotional offer. If you're informed, you may be able to negotiate a rate closer to the base approved by the lender for your credit tier.

How Market Conditions Affect the Money Factor

Money factors are also influenced by economic and market conditions. Leasing companies adjust rates based on:

- Interest rates: Benchmarks set by the Federal Reserve or other central banks directly influence lease rates.

- Inflation: Higher inflation generally leads to higher lease interest rates, increasing total lease costs.

- Leasing company policies: Captive finance companies (those owned by car manufacturers) often offer better money factors to customers with strong credit.

- Residual value: Vehicles that retain their value well (i.e., low depreciation) usually qualify for lower money factors because they pose less risk to the lender.

Can You Influence the Money Factor?

A dealer cannot lower the money factor below the "buy rate" — the base rate set by the bank or leasing company. However, there are several strategies you can use to secure the lowest possible MF:

- Improve your credit score (e.g., by reducing debt and making timely payments)

- Make MSDs – Multiple Security Deposits (each refundable deposit typically reduces the MF by about 0.00005)

- Use promotional lease offers, if available

- Negotiate the MF with the dealer — ask for the minimum rate allowed by the lender for your credit tier

For some leasing offers, you may be given a very attractive interest rate, but with one caveat: the entire amount of the lease must be paid in a single payment.

What Is a Good Money Factor on a Lease?

One quick way to evaluate a lease money factor is to look at the first few digits after the decimal point. Here’s a general guide to understanding money factors and their equivalent APR ranges:

| Money Factor | Equivalent APR | Rating | Typical Credit Tier (FICO) |

|---|---|---|---|

| .00100 | 2.40% | Excellent Deal | 750+ (Tier 1) |

| .00125 | 3.00% | Very Good | 700–749 (Tier 2) |

| .00175 | 4.20% | Average | 660–699 (Tier 3) |

| .00250 | 6.00% | High | 620–659 (Tier 4) |

| .00300+ | 7.20%+ | Very High | Below 620 (Tier 5) |

When comparing lease deals, always check the money factor to gauge how competitive the financing terms are. Even a small difference — say, 0.0005 — can result in hundreds or thousands of dollars over the life of a lease.

For example, using the earlier case with a money factor of 0.00236, the deal would fall in the “Good” to “Fair” range. It's not the cheapest, but also not inflated. With a strong credit score, it might be possible to qualify for a rate closer to 0.0015–0.0020, which is roughly 3.6%–4.8% APR.

Want to evaluate your lease offer? Use our AI-powered tool — Car Lease Agreement Analyzer — to instantly check whether your deal is competitive.

Why Understanding the Money Factor Matters

To make a financially sound leasing decision, it’s crucial to understand how credit works. Lenders adjust the money factor based on your credit score, lease term, and vehicle type. Knowing how the money factor works gives you a significant advantage for several reasons:

- Negotiating Power: Helps you determine whether the lease rate is fair

- Cost Comparison: Makes it easier to compare lease vs. financing offers

- Financial Planning: Affects your total interest cost and monthly payment

- Transparency: Helps you avoid hidden markups or financial traps

As a lease customer, understanding the money factor gives you the leverage to negotiate better terms. It also empowers you to make a more informed choice between leasing and other financing options.

Final Thoughts

Grasping the concept of the money factor is key to making smart financial decisions when leasing a vehicle. While it may seem like just a small decimal number, its impact on your monthly payments and total lease cost is significant.

By learning how to calculate the money factor, using a money factor lease calculator, and understanding what counts as a fair rate, you can minimize the cost of your lease deal.

When comparing lease offers, don’t focus only on the monthly payment. Instead, examine the money factor alongside the APR, estimate the total cost, and don’t be afraid to ask questions.

Knowledge is your most powerful tool when leasing a car. The more you understand the numbers — especially the money factor — the better deal you’ll get.

Frequently Asked Questions

What does the money factor indicate in a lease?

It’s the decimal form of the interest rate you’re paying. It determines how much interest you pay each month and is essential when evaluating lease deals.

How do I convert the money factor into a familiar percentage?

Multiply the money factor by 2400. For example, a MF of 0.003 equals a 7.2% APR.

Can I negotiate the money factor in a lease deal?

Yes. Ask for the “base buy rate” and avoid unnecessary markups. Use MSDs (Multiple Security Deposits) if the lease provider allows them.

What is considered a good money factor for a car lease?

Anything at or below 0.00125 (equivalent to 3% APR) is typically considered excellent. Higher numbers indicate more expensive financing.

Is there a tool to calculate or compare money factors?

Yes. You can use our Money Factor to APR Calculator, or plug values into a spreadsheet to compare the total cost between multiple offers.

Trending post

1

4