Apr 01, 2025

Car Lease Agreement: Sample Contract with Explanations

May 01, 2025

Car Lease Contract — Agreement, which defines the terms of payment and use of a vehicle for a certain period of time (usually 2 - 4 years). At the same time, there are no rights to own the car, the car is the property of the leasing company or bank. Lease is an alternative to purchase for personal and business use.

But for first-time lessees, a vehicle lease agreement can be confusing. It includes unfamiliar terms, hidden conditions, and strict limitations. Understanding how much you’ll pay, how far you can drive, and what you can (or can't) do with the vehicle is essential before deciding whether leasing makes sense — or if buying would be the better option.

What You’ll Learn:

- What a car lease agreement is and how it looks

- What’s included in the contract

- Items not included in the contract

- Common lease restrictions

- What happens when your lease ends

- Key details to watch out for

Before signing a car lease agreement, make sure you fully understand key terms such as residual value, money factor, and mileage allowance. You should also be clear on the monthly payments, car lease fees, and any additional costs like the acquisition fee or disposition fee. Knowing these leasing basics can help you avoid costly mistakes and make an informed financial decision.

What Is a Vehicle Lease Agreement?

Lease to Own Car Agreement is a contract between the lessee and the lessor that allows the lessee, for a certain fee, to use the vehicle for a certain period of time. The lessee has no right of possession and is responsible for insurance, maintenance and technical condition of the vehicle.

Contracts from different dealerships and finance companies may differ in their terms in some details, but contain common elements. Some are easier to understand, some are more complicated. Therefore, it is important to read each clause of the agreement carefully before signing the deal.

A vehicle lease agreement outlines the terms, monthly costs, term, restrictions and additional fees. Such an agreement can be made with any vehicle that has a vehicle identification number (VIN). The most common vehicles are new or used cars or trucks.

Using an agreement protects the parties from any misunderstandings or miscommunications that may occur during the lease term. Although leasing allows you to drive a new car at a lower price than buying it, you can expect unexpected costs, potential penalties, and hidden fees.

What Does a Car Lease Agreement Look Like?

The first sections of a lease agreement usually outline the total lease amount, due-at-signing costs, and how your monthly payments are calculated. Later sections include details on early termination policies, wear-and-tear penalties, end-of-lease options, and more.

Here are the core sections typically found in a lease agreement:

- Amount due at signing

- Monthly lease payment

- How the monthly payment is calculated

- Total number of payments

- Additional costs or fees

- Total finance charge (if applicable)

- Early termination policy

- Explanation of excessive wear charges

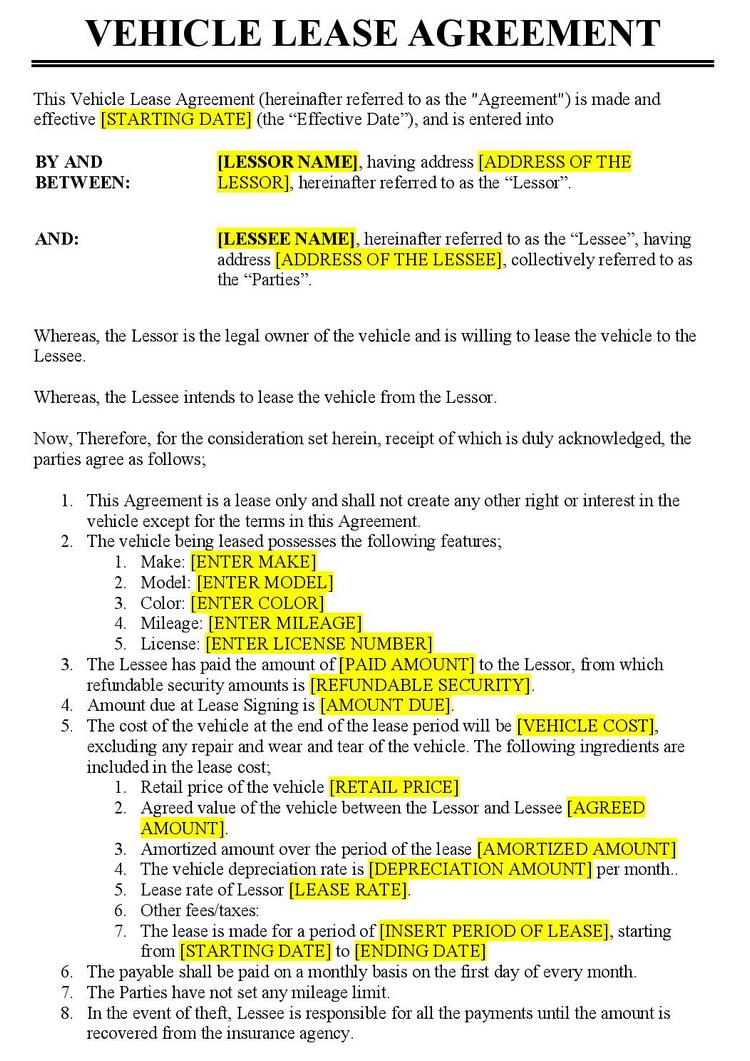

How the vehicle lease agreement template looks like is shown in the picture below:

Tip: Ask for a Sample Lease Contract

Before committing to a deal, ask the dealership for a blank sample lease agreement. This gives you time to review the structure, understand what each section means, and compare it against other offers.

Consumers have the right to request a lease agreement template before signing the deal. Under FTC rules dealers provide information on key lease terms, including down payment, monthly payments, and additional fees.

Many leasing companies use their own customized versions of standard lease agreement templates, but they all include the key elements outlined above.

What’s Included in a Car Lease Contract?

Under the Consumer Leasing Act (Regulation M), leasing companies are federally required to disclose key terms before you sign a lease. While that might sound like strong consumer protection, there’s one big catch: they’re not required to show the actual APR. The total amount of interest that will be paid for the entire term of the lease is considered sufficient. This is a significant disadvantage that complicates the analysis of the deal.

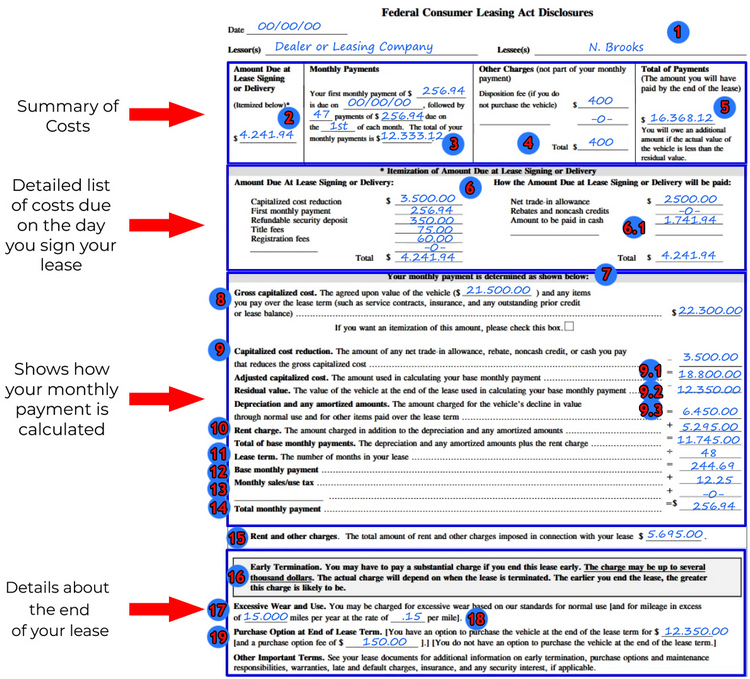

To help you understand how lease expenses are calculated, we’ve included a sample lease image that breaks down the key sections. Car lease fee explained under each section.

Here’s what you’ll typically find in a standard lease agreement:

- Lessee and Lessor Info

Names of the person leasing the car and the leasing company or dealership. - Amounts Due at Signing

The total amount you’re required to pay when you sign the lease — includes cash, trade-in equity, or incentives. - Monthly Payment Terms

Your monthly lease payment, the number of payments (months), and the total amount you’ll pay in monthly charges. - Other Charges

These may include fees like the disposition fee (charged at the end of the lease), which are not part of your monthly payment. - Total of Lease Payments

The total dollar amount you’ll pay over the lease term, not including refundable deposits or DMV/registration fees. - Details About the Amount Due at Signing

6.1 Payment Breakdown

An itemized explanation of how the due-at-signing amount is calculated. This should match the figure in section 6. - How Monthly Payments Are Calculated

- Gross Capitalized Cost

This is the vehicle’s selling price plus additional items such as warranties or insurance, and sometimes includes negative equity from a previous loan. - Capitalized Cost Reduction

Anything that lowers the amount being financed — includes down payments, trade-in credits, or rebates.

9.1 Adjusted Capitalized Cost

The amount being financed over the term of the lease. It’s the gross cap cost minus any cap cost reductions.

9.2 Residual Value

The estimated value of the vehicle at the end of the lease — and the price you’d pay if you decide to buy the car when the lease ends.

9.3 Depreciation

The difference between the adjusted cap cost and the residual value — what the car is expected to lose in value over the lease term. - Rent Charge

This is essentially the finance charge, calculated using a money factor, which depends on your credit score. Note: the actual money factor may not be disclosed in the contract. - Lease Term

The duration of the lease in months — the number of monthly payments you’re expected to make. - Base Monthly Payment

The cost of leasing the car before taxes and fees. - Sales/Use Tax

Taxes added to your monthly payment — varies by state. - Total Monthly Payment

Your final monthly cost, including taxes, registration, and other applicable charges. - Total Lease Cost

The full cost of leasing the vehicle over the entire lease period (Base Rent + Operating Costs). - Early Termination

Explanation of what happens if you break the lease early — including penalties or outstanding balances. - Excess Wear & Tear and Mileage

Details on mileage limits (usually annual), and what happens if you exceed them or return the car with damage. Modifications may also be prohibited. - Excess Mileage Fee

The cost per mile over your allowed mileage — typically between $0.15–$0.25 per mile. - Purchase Option Price

The amount you’d need to pay if you want to buy the vehicle at the end of the lease term.

Need a Lease Template?

You can download a sample lease agreement in PDF format on our website. For a customizable document, try using platforms like Wonder.Legal or similar tools to create a personalized Vehicle Lease Agreement that suits your needs.

What’s Not Included in a Car Lease Contract?

Even though lease agreements are designed to provide transparency, there are a few important details that typically won’t appear in black and white:

No Interest Rate (APR) Disclosure

Your lease contract won’t show an actual interest rate. Instead, it will reflect your finance charges as a "rent charge", calculated using a money factor — a decimal number that’s often not disclosed. The only exceptions are special promotional offers that provide for a reduced or zero interest rate.

Acquisition Fee Not Listed Separately

Most lease agreements won’t itemize the acquisition fee (sometimes called a lease origination fee). Instead, this fee is usually bundled into the gross capitalized cost of the vehicle. You’ll only see it separately if you’re paying it upfront in cash.

No Specific Early Termination Cost

Lease contracts usually include only a general explanation of early termination penalties. Why? Because the exact amount depends on multiple variables: how far you are into the lease, how much you’ve paid so far, and how the car’s value compares to what you still owe. This is the information your leasing company can provide when you terminate the deal. You can find out more about this on the CFPB website or from a lawyer who specializes in auto law in your state. What you should know — is that the sooner it happens, the more expensive it will be.

Common Lease Restrictions You Should Know About

In part of the agreement, there is an explanation of the restrictions placed on the use of the vehicle. The rules include mileage limits and penalties for early termination. Therefore, you should read all pages of the agreement carefully. These rules are governed by both the agreement itself and state law. To better understand your local leasing laws, visit your state’s DMV website or legal resources like Nolo.com.

Here are some common limitations to watch out for:

Vehicle Modifications: Since you don't actually own the car, there are certain restrictions on its use. A large number of modifications are prohibited (e.g. painting, changing the stereo, suspension).

Excessive Wear and Tear: You must return the car in normal condition at the end of the lease. Read the section that tells you what condition you must keep the vehicle in.

Maintenance: Any vehicle needs periodic maintenance. Read the section of your agreement that states your responsibility to maintain the vehicle and cover the cost of repairs.

Mileage: The agreement contains a certain number of miles you are allowed to drive each year at no extra charge (these are built into the vehicle's depreciation).

What Happens at the End of a Car Lease?

A lease gives you the right to use a vehicle for a limited period of time, but ownership remains with the lessor. When the lease term ends, you typically have three options:

- Return the vehicle and walk away.

- Lease a new vehicle.

- Purchase the vehicle at the pre-determined residual value.

As you approach the end of your lease, evaluate the pros and cons of each option and prepare accordingly. Keep in mind that if you choose not to lease again, you may be charged a disposition fee. There are also a few other important considerations.

Lease-End Pitfalls to Watch For

When signing a lease, it’s crucial to be aware of potential pitfalls that could lead to unexpected expenses. These fall into three main categories:

- Excess wear and tear charges

- Excess mileage fees

- Early termination penalties

Lessee concerns often focus on wear-and-tear policies. Charges may apply if the vehicle is returned with damage deemed excessive, or if unauthorized modifications have been made — the vehicle must be returned in factory condition. If you selected a mileage allowance that doesn’t match your driving needs, you'll pay for the extra miles. And if you terminate the lease early, substantial penalties may apply based on how much time remains on the lease.

Additionally, most lease agreements require you to carry full coverage auto insurance, just like with a car loan. Without GAP insurance, if the vehicle is stolen or totaled, you could still be liable for significant costs — just as described above.

Why Should You Know All This?

Because lease contracts are sometimes written with errors. Your legal protections are limited — only clear fraud can lead to litigation. There is no "cooling-off" period or automatic right of cancellation within three days. That’s why you must double-check every part of the contract yourself before signing.