Apr 01, 2025

Car Leasing Mistakes to Avoid: How to Lease Smart and Save Thousands

May 21, 2025

Leasing a new car can be a great way to drive the latest model paying just a fraction of its full price. But there are hidden pitfalls that can cost you thousands if you're not careful. Want to avoid the most common leasing mistakes and approach it like a pro? Then this article is for you.

You’ll learn:

- The pros and cons of leasing

- Common car leasing mistakes to avoid

- A proper step-by-step leasing plan

- Tools and resources to help you lease smarter

- Final thoughts

Pros and Cons of Leasing

Leasing a car in the U.S. is a great option, especially for those who want to drive a new vehicle every few years and prefer lower monthly payments. However, leasing isn't for everyone. Alongside the benefits, there are some drawbacks that could influence your decision.

Pros of Leasing:

- Lower monthly payments

- Drive a new car more often

- Often includes warranty and maintenance

- Lower upfront costs (down payment), although this depends on the deal

Cons of Leasing:

- You don’t own the vehicle

- Limited mileage (typically 10,000–15,000 miles per year)

- Strict usage terms

- Early termination fees

- You must return or buy the car at the end of the lease term

“Why is leasing a car a bad idea?” — It’s not, as long as you do everything right. But many people make mistakes that turn leasing into a financial trap.

The Most Common Car Leasing Mistakes

I’ve identified 9 of the most frequent (and costly) car leasing mistakes. Here they are — and how you can avoid them:

1. Not Negotiating the Price

Many people believe that the price of leasing is non-negotiable, so they completely refuse to negotiate the price. That’s a mistake. At the deal stage, you should negotiate the trade-in value (if you’re trading in a vehicle), dealer fees, and any additional services. You can even negotiate the mileage allowance ahead of time if you expect to drive more than the standard limits.

Tip: Always negotiate the capitalized cost (selling price) the same way you would if you were purchasing the vehicle. Dealers often try to focus your attention on the monthly payment instead of the gross capitalized cost. Do your research in advance so you know the fair market price of the car you're interested in.

Example: Reducing the capitalized cost by $2,000 could lower your monthly lease payment by $55–60.

2. Putting Too Much Money Down

A common trap is making a large upfront payment just to get a lower monthly rate. Why is this risky? If the vehicle is totaled or stolen early in the lease, you could lose that down payment and still be left without a car.

Recommendation: Don't pay too much money up front. Try to keep your initial outlay under $2,000, or better yet, find a “sign and drive” leasing option.

3. Underestimating Your Mileage Needs

Underestimating mileage is an expensive mistake. Standard leases typically include 10,000–12,000 miles per year. Exceeding that limit can cost you $0.15–$0.25 per mile. Some deals offer 15,000 miles, but the monthly payment will be higher.

Tip: Consider not only your daily commute but also road trips and business travel — these are often the reason for going over the limit. Be honest with yourself. If you regularly drive over 1,000 miles per month, negotiate a higher mileage allowance in advance.

4. Not Maintaining Your Vehicle

Leased vehicles must be returned in “reasonable condition.” What does that mean? — You’re expected to drive carefully and keep the car in good shape. Neglecting maintenance of the car, frequent small bumps with foreign objects of the body and eating in the interior of the car will turn out to be additional expenses for you.

What counts as excessive wear and tear:

- Scratches longer than 4 inches

- Worn-out tires

- Stained interior

Solution: Stick to the recommended maintenance schedule. Get a pre-inspection if it’s available. Prepare the vehicle for the lease-end inspection to avoid excess wear and tear charges. Returning a vehicle with major scratches or dents could result in you being charged the full retail cost of repairs.

Also, be aware that you'll be charged for reversing any modifications you've made that are not allowed under your lease.

5. Leasing a Car for Too Long

Manufacturer warranties often expire on leases longer than 36 months.

Why this is bad: You’ll be responsible for any repairs and maintenance yourself. A 48- or 60-month lease increases the risk of being stuck with costly out-of-pocket repairs once the warranty ends.

Practical tip: The ideal lease term is 24 or 36 months. This helps you stay under warranty and avoid unexpected expenses.

6. Ignoring GAP Insurance

If your leased car is totaled or stolen, you might owe more than your standard insurance covers. The insurance company pays the car’s actual value — but you still owe the remaining lease payments.

Solution: Make sure GAP (Guaranteed Asset Protection) insurance is included in your lease or purchase it separately. GAP covers the difference between what you owe and what the car is worth. It protects you from having to pay out of pocket for a totaled car.

Helpful note: Adding GAP to your existing auto insurance policy is usually cheaper than getting it through the leasing agent.

7. Trusting “Low Monthly Payment” Ads

Don’t fall for advertised low monthly payments. Many promotions claim lease offers for $199/month, but require $3,999 due at signing — and the term is often just 24 months.

| Term | Value |

|---|---|

| Monthly Payment | $199 |

| Lease Term | 24 months |

| Down Payment | $3,999 |

| Total Cost | $8,775 |

These eye-catching deals are usually only available to those with excellent credit. Even with an average FICO score, you’ll likely face a higher money factor (equivalent to an interest rate) and more restrictive lease terms.

Always do the math: Total lease cost = (Monthly payment × Term) + Fees + Down payment

Hidden pitfalls: The low monthly payments promoted in ads are misleading if you don’t read the fine print. And as for your actual APR (annual percentage rate), you’ll only understand it by calculating the total interest paid over the life of the lease.

8. Skipping the Down Payment Entirely

While a large down payment is risky, if not making a down payment will result in higher monthly payments.

The key is balance: Aim for a modest down payment — just enough to keep your payments manageable without exposing yourself to significant financial loss. Your monthly lease payments are partially based on the amount financed after the down payment. Even a small initial payment can significantly reduce your total lease cost.

9. Ignoring Residual Value

The amount on which the lease is based is the capitalized cost. It includes interest and fees less the residual value of the vehicle. The bigger the gap between the capitalized cost and the residual value, the higher your payments will be.

Tip: To keep your monthly payments lower, look for vehicles with high residual values at the end of the lease term. These are often models with strong manufacturer incentives or lease support.

Important note: This becomes a mistake only if you plan to buy the car at the end of the lease — the buyout price will be based on that higher residual value. It makes sense to purchase the car only if the buyout price is below its actual market value at that time.

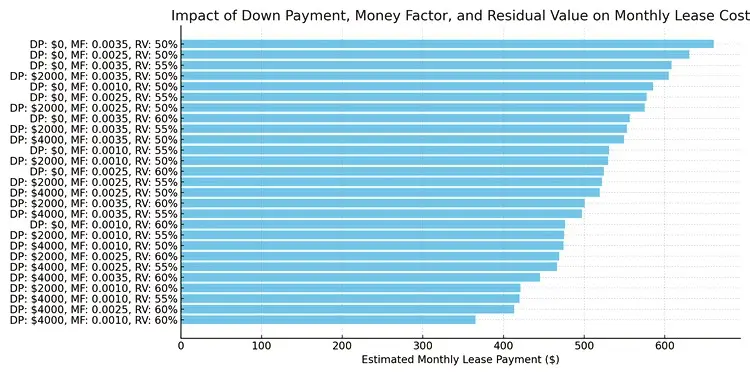

How Different Lease Factors Impact Your Monthly Payment

The chart below illustrates how your monthly lease payment changes depending on three variables: residual value, down payment, and money factor (lease interest rate).

You can easily calculate this yourself using our Lease Down Payment Calculator.

Lease Smarter: Step-by-Step Guide

Use this checklist to lease with confidence:

Step 1: Know Your Budget

- Determine how much you can afford both monthly and upfront.

- Use a lease calculator to estimate your payments.

Step 2: Choose the Right Vehicle

- Look for models with high residual values (lower depreciation = better lease terms).

- Compare lease offers from different dealerships.

Step 3: Get Lease Quotes from Multiple Dealers

- Compare money factor, residual value, monthly payments, and fees.

- Check your credit score beforehand.

Step 4: Negotiate the Lease Price

- Approach it like a purchase — negotiate the selling price first, then talk about lease terms.

Step 5: Verify Mileage Limits

- Make sure your annual mileage cap fits your driving habits.

- If needed, buy extra miles upfront — it’s cheaper than overage penalties. You can even negotiate a refund clause for unused miles (make sure that’s in the contract).

Step 6: Review the Lease Agreement Carefully

- Check for disposition fees, early termination penalties, and wear-and-tear policies.

- Identify any hidden costs or conditions.

Step 7: Confirm GAP Insurance Coverage

- Ask whether GAP insurance is included in the lease. If not, purchase it separately from your insurance provider.

Step 8: Maintain the Vehicle Properly

- Follow the maintenance schedule.

- Avoid stains, dents, or any major damage.

Step 9: Plan for Lease-End Options

- Decide in advance whether to lease a new car, return the vehicle, or buy it.

- Compare the residual value to market value before making a buyout decision.

- Look for loyalty or lease-end incentives.

Tools and Resources to Help You Avoid Leasing Mistakes

Here are trusted resources that will help you compare offers, calculate lease costs, and understand contract terms:

| Tool | Purpose | Link |

|---|---|---|

| Edmunds Lease Calculator | Estimate the full cost of a lease | edmunds.com |

| TrueCar Lease Deals | Compare lease offers across the U.S. | truecar.com |

| Credit Karma Auto Tools | Compare lease vs. purchase based on your credit score | creditkarma.com |

| Leasehackr Forum | Community sharing top lease deals and strategies | forum.leasehackr.com |

| Autotrader Lease Guide | Learn lease terminology and the process | autotrader.com |

| Lease Mileage Tracker | Free Excel tool to track your lease mileage | practicalspreadsheets.com |

Our own helpful tools to make your lease decision smarter:

Final Thoughts

Leasing can be a smart financial move — if you know what you’re paying for and avoid common mistakes. Here are key principles to remember:

- Always negotiate a lease like you would a purchase

- Know your mileage and driving habits

- Read every line of the contract (after learning the terminology)

- Compare several offers before signing anything

- Plan ahead for the end of your lease: return, buy, or trade in

If you found this article helpful, share it with friends or save it for later!