Apr 01, 2025

Should You Lease a Car with $0 Down? Revealing the reality of the offer

May 30, 2025

Leasing a car without a down payment sounds attractive, doesn't it? But what does such a deal really imply, is it available for all comers and is it really worth it for you to conclude such a contract? I offer to find out the whole truth about car leasing with zero down payment, to understand what are the advantages and disadvantages of such an offer, what hidden costs may be waiting for you, and also to find out whether it is profitable for you.

After all, while "zero down payment" leasing often means there is no down payment, it doesn't mean you'll pay $0 when you sign the contract. It just means that you do not contribute money that reduces the capitalized value of the car (Cap Cost Reduction).

In this article, I will explain:

- What Does "Zero Down" Really Mean?

- How is Your Down Payment Used in Leasing?

- What Does a Zero-Down Payment Include?

- How Does Down Payment Affect Leasing?

- How Down Payment Affects Monthly Payments?

- Pros and Cons of the Zero Down Offer

- Should You Make a Down Payment on a Lease?

- Helpful Tools to Explore Lease

- Final Conclusions

What is a Zero Down Payment Lease?

Zero down payment leasing (also called $0 down payment leasing) is a car leasing offer that allows you to sign a contract without making a traditional down payment. At first glance, this may seem like a great deal — you drive away in a new car without paying thousands up front. But in reality, that's not entirely true and the offer doesn't prove to be relevant for everyone who wants it.

In most cases, you will still have to pay other upfront fees such as registration, acquisition fee, first month's payment and taxes. The term "zero down payment" usually means no capitalized reduction in value, not a zero down payment when you sign the contract. Plus, you'll learn about additional terms and conditions at the table when you read the contract.

What Happens to the Down Payment on a Leased Car?

Your car lease down payment will be used to cover certain financial obligations:

- Reducing the size of your monthly payments.

- Covering fees.

- Providing solvency.

By making a down payment on your lease, you reduce the marginal cost of the vehicle.

What’s Typically Included in a "$0 Down" Lease Offer?

| Cost Component | Accounted for in "$0 Down"? | Notes |

|---|---|---|

| Capital Cost Reduction | ✓ Not available | Rent is not reduced |

| First Month's Payment | ✖ Required | Always payable at signing |

| Acquisition Fee | ✖ Required | Amount can be $495–955 |

| Registration/Title/Doc Fees | ✖ Required | Depends on state |

| Sales Tax | ✖ Required | Often due upfront or rolled into monthly payments depending on the state |

| Security Deposit | ✖ Not Always | Sometimes required for low credit score |

How Leasing With Down Payment Works?

To understand how down payment works let's look at the example of a 36-month lease on a $36,000 car with a residual value of 58% and a cash factor equivalent to 5% APR. See the table for a comparison of lease terms at $0 and $3,000 down payment:

| Lease Terms | With $0 Down | With $3,000 Down |

|---|---|---|

| Capitalized Cost | $36,000 | $33,000 |

| Residual Value | $20,880 | $20,880 |

| Depreciation | $15,120 | $12,120 |

| Finance Charge | ~$2,160 | ~$1,980 |

| Monthly Payment | ~$480 | ~$395 |

| Total Cost | ~$17,280 | ~$17,220 |

As you can see, the down payment lowers your monthly costs, but the overall savings are not as significant as often thought. Plus, there is a downside — your initial risk increases.

Bottom line: You save ~$60 per month, but you take on initial risk. If the car gets into an accident or is stolen early, your $3,000 down payment could be lost.

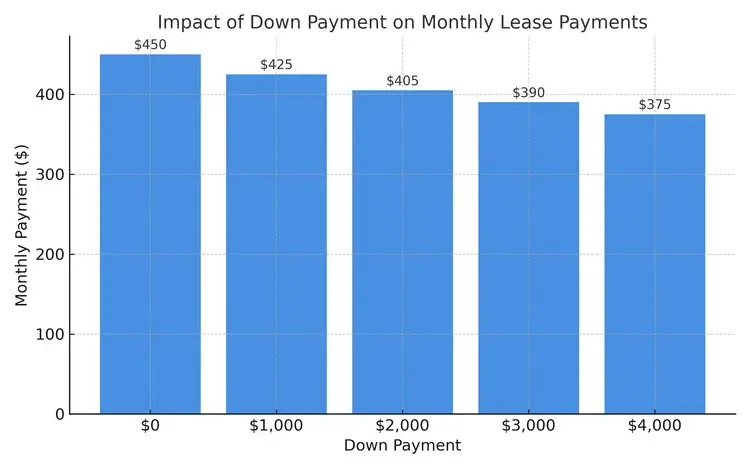

Chart: How Down Payment Impacts Monthly Lease Payment

Example: MSRP $36,000 | Term: 36 months | Residual $21,000 | MF: 0.00125

Your savings: a zero down lease cost will be $75 per month more than if you made a $4,000 down payment.

You can see how a certain amount of cash advance will change the amount of your monthly payments by using this tool:

Pros and Cons of Zero Down Leases

| Pros | Cons |

|---|---|

| Lower upfront costs | Higher monthly payments |

| Easier entry for low-cash buyers | More total paid over the lease term |

| Easier to walk away financially | Increased risk if car is totaled or stolen |

| Often include incentives | More difficult credit qualification |

| Less risk if vehicle is totaled early | May not qualify for all promotional deals |

Leasing without advance payment is a good solution for those who want to reduce start-up costs. But remember: it will cost more in the long run. The main thing is to understand your priorities: low payment or lower risk of losing money.

When Does a Down Payment Make Sense?

A $0 down payment offer (with GAP insurance included) may be more advantageous when you need maximum flexibility and low risk.

It is not necessary, but it will be helpful to make a down payment in these cases:

- Your credit score is below 680 and you want to improve your chances of lease approval.

- You want to stay within your target monthly budget.

- You are leasing an expensive vehicle and plan to keep it for the long term.

Avoid a large down payment if:

- You are leasing a vehicle that could depreciate quickly.

- You fear a total loss (accident or theft) — you may not get your down payment back.

- You plan to trade-in or transfer the lease at a later date.

You should also keep in mind that there is no capital accumulation. Unlike purchase financing, leasing does not result in capital formation, so the down payment does not contribute to ownership.

Tools to Compare Lease Offers

| Tool | What It Does | Link |

|---|---|---|

| Lease Down Payment Calculator | Compare $0 vs $2,000 down scenarios side by side | lease-vs-buy.com |

| Edmunds Lease Calculator | Full lease payment breakdown with fees | edmunds.com |

| TrueCar Lease Deals | Comparison of national leasing offers | truecar.com |

| Leasehackr Calculator | Evaluate money factor, taxes, residual values | leasehackr.com |

| Credit Karma Auto Tools | Compare lease vs. loan based on credit score | creditkarma.com |

Final Thoughts

Zero down leases payment are suitable for those who are looking to minimize initial costs and prefer short-term use of the vehicle, but be careful:

The total cost will be higher

Ads may conceal real down payments

GAP insurance is mandatory

Always read the fine print and calculate the total cost of the lease, not just the monthly payment. Use the tools listed above to compare real offers.

Want to know what's best for your lifestyle and budget?

👉 Try our interactive lease-to-buy comparison tool to make an even smarter choice.